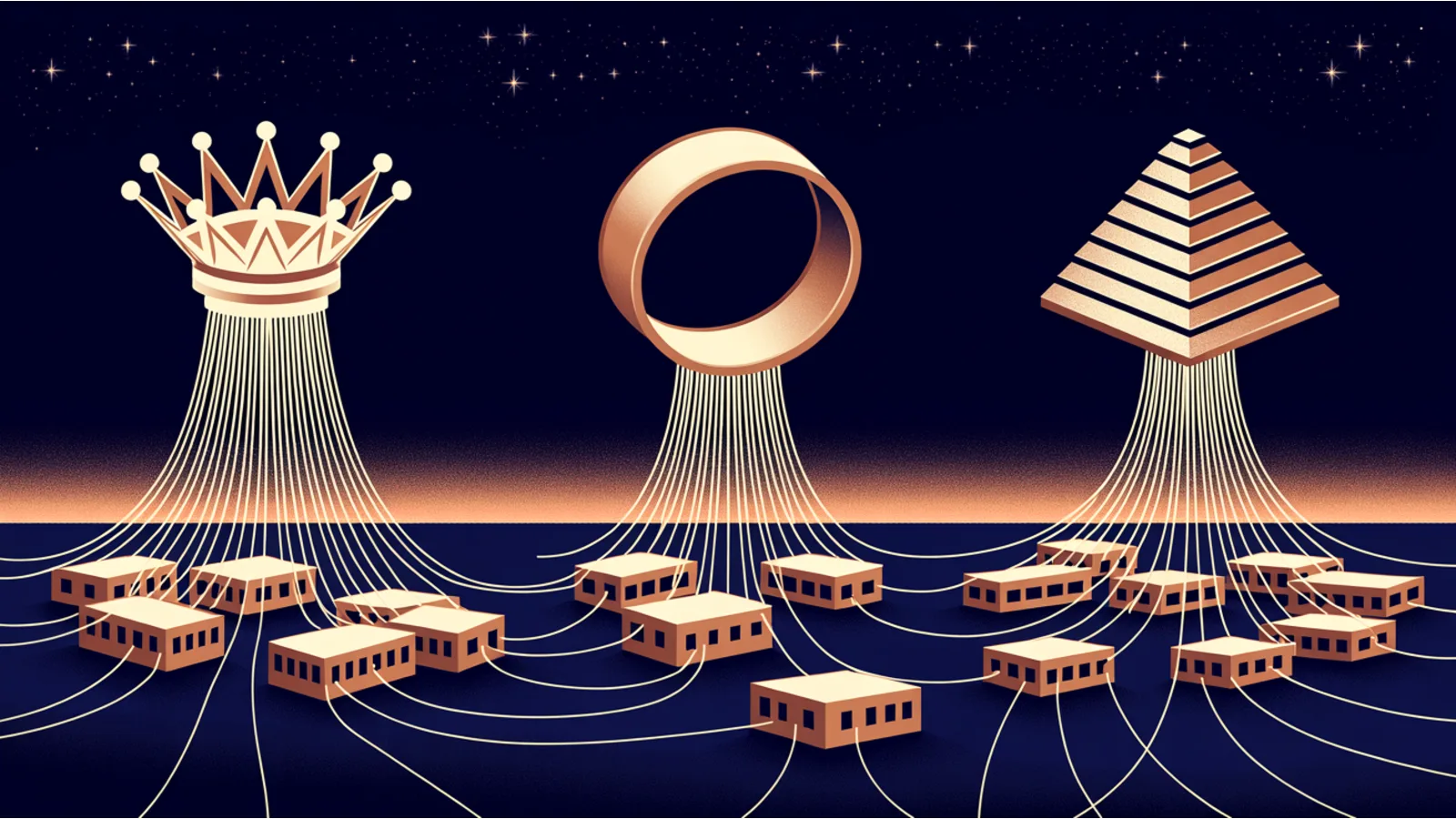

An earlier piece in this series looked at how Sweden's Wallenberg family controls much of a national economy not by owning it but by placing foundations at the top of a holding structure. That trick is not Swedish. Three of the largest private empires on earth, India's Tata, Sweden's IKEA, and Italy's Agnelli family, are each built on a version of the same idea: put an entity at the very top that no single heir can sell and no outside buyer can seize, hand it a minority of the economic stake but a majority of the votes, and the empire outlives everyone inside it. The legal wrappers differ, and one important distinction has to be drawn honestly, but the mechanism is the same. Here is how each one works, from the record.

Tata: charitable trusts that own the holding company

The Tata group, founded in India in 1868, is that country's largest conglomerate, a sprawl of 31 companies with aggregate revenue of more than $180 billion in the 2024 to 2025 financial year and a combined market value of its listed arms above $328 billion (Tata). Its financial engine is Tata Consultancy Services, India's largest IT firm, which alone earned about $30 billion in revenue and supplies the bulk of the dividends that flow up the structure (TCS). The empire also owns Jaguar Land Rover, bought from Ford in 2008, and the former Corus steelworks, bought in 2007 (Jaguar Land Rover; Tata Steel).

The control structure is the point. At the top of the group sits Tata Sons, an unlisted holding company, and Tata Sons is itself controlled by the philanthropic Tata Trusts, which hold about two-thirds of its stock, roughly 66 percent, chiefly through the Sir Dorabji Tata Trust and the Sir Ratan Tata Trust (Tata Trusts). The dividends that TCS and the other companies send up to Tata Sons flow onward to these charitable trusts, which deploy them on hospitals, education, and research while retaining voting control of the whole empire. It is the same loop the Wallenberg foundations run: permanent control converted into permanent philanthropy. Ratan Tata, who chaired both the group and its main trusts and so embodied the union of empire and charity, died in October 2024; Noel Tata succeeded him as chairman of the Tata Trusts, while N. Chandrasekaran has chaired Tata Sons since 2017 (Al Jazeera; Business Standard). The structure's grip was tested in 2016, when the group ousted chairman Cyrus Mistry, a fight the Indian Supreme Court ultimately resolved in Tata's favor in 2021 (iPleaders case analysis). The Mistry family's Shapoorji Pallonji group, the largest minority owner of Tata Sons at about 18 percent, has pushed for the holding company to go public, a listing the trusts have resisted precisely because it would loosen their control (Forbes India).

IKEA: the company that owns itself

IKEA takes the same idea to its logical extreme. Ingvar Kamprad founded the company in Sweden in 1943 at the age of seventeen, and before his death in 2018 he engineered an ownership structure designed so that IKEA could never be sold, inherited, or broken up (Wikipedia, "Ingvar Kamprad"). It comes in two deliberately separated halves. The retail business, which runs the stores, is owned by Ingka Holding, which is in turn owned by the Stichting INGKA Foundation, a Dutch foundation that, in the words of the group itself, has "no owners" (Ingka). Ingka is the largest IKEA franchisee, accounting for the great majority of global IKEA sales, with revenue of about 41.5 billion euros in its 2025 financial year (Ingka). The brand itself is held separately: Inter IKEA Systems owns the IKEA concept and collects a franchise fee of 3 percent of net sales from every store, and since 2023 it has been owned by a separate Inter IKEA Foundation in Liechtenstein (Inter IKEA; Inter IKEA Foundation).

The crux is that a foundation of this kind, a stichting, has no members and no shareholders. It "owns itself," which is exactly why IKEA cannot be bought, cannot be split among heirs, and cannot be taken over (Wikipedia, "Stichting INGKA Foundation"). The design also minimizes tax, and it has drawn scrutiny for it: a Swedish investigation estimated the structure saved Kamprad billions in tax over two decades, and in 2017 the European Commission opened a state-aid investigation into the Netherlands' tax treatment of the brand arm (The Local; European Commission). The Kamprad family does not own IKEA in any ordinary sense; by design it is capped at a minority of foundation board seats, with Kamprad's sons holding a limited, deliberately constrained role (Ingka Foundation governance). The famous "world's wealthiest foundation" figure of about $36 billion comes from a 2006 estimate and is now dated, since the foundation no longer discloses its assets, so it is best cited as a historical benchmark rather than a current number.

Agnelli: the holding-company pyramid

The Agnelli family reaches the same destination by a different legal road, and the difference matters enough to state clearly: this is not a foundation. Giovanni Agnelli co-founded Fiat in Turin in 1899, and today the roughly two hundred descendants control the empire through a pyramid of holding companies rather than a charitable trust (Exor; Wikipedia, "Agnelli family"). The family owns a private Dutch holding company, Giovanni Agnelli B.V., which controls the listed investment company Exor, and it does so through special voting shares that convert a minority of the money into a supermajority of the votes: about 55 percent of Exor's economic rights but roughly 84 percent of its votes (Exor ownership structure). Above even that sits Dicembre, the personal vehicle of John Elkann, the great-great-grandson of the founder, which holds the largest block of the family holding company and puts him at the apex of the pyramid (SEC filing).

Through Exor, the family controls a remarkable spread of companies while owning only a minority of most of them, again by leaning on enhanced voting rights. Exor is the largest shareholder of Ferrari (about 20 percent of the capital but roughly 32 percent of the votes) and of Stellantis, the merged Fiat-Chrysler-Peugeot group, and it holds large stakes in the farm-equipment maker CNH, the Juventus football club, Philips, and The Economist (Wikipedia, "Exor"). In a neat crossover with the first empire in this piece, Exor agreed in 2025 to sell its truckmaker, Iveco, to India's Tata Motors (GlobeNewswire). One correction worth making, because it is widely muddled: John Elkann is the chief executive of Exor, not its chairman; he is separately the chairman of Stellantis and of Ferrari (Exor). Exor reported a net asset value of about 33 billion euros at the end of 2025, and the family's collective wealth is estimated near $14 billion, far larger than Elkann's personal fortune, which should not be confused with it (Exor NAV; Bloomberg).

The common mechanism

Read together, the three empires are three answers to one question: how do you keep something enormous whole across generations and out of the reach of heirs, rivals, and the taxman? The answer, in every case, is to put an apex entity at the top that cannot easily be cashed out or bought, and to give it control rights that far exceed its economic stake. Scholars call the charitable version an "enterprise foundation," a foundation that owns a company, self-governing and ownerless, exercising control through voting rights rather than dividends, and the research finds such firms tend to be unusually long-lived and long-term in their decisions (enterprise foundation research). Tata is the purest example, charitable trusts owning two-thirds of the holding company and turning its dividends into philanthropy. IKEA is the most extreme, a double-foundation structure that makes the company literally ownerless and, by its founder's intent, unbuyable and lightly taxed. Agnelli is the sibling case, the same effect achieved not through a foundation but through a family holding company stacked with loyalty shares, a distinction worth keeping straight even as the result converges.

The neat line is that these are three families, in three countries, running one trick. Put an entity at the top that no heir can sell and no rival can buy, give it a minority of the shares but a majority of the votes, and the empire outlives everyone in it. In Tata's case that top entity gives its income to charity. In IKEA's case it answers to no one at all. In Agnelli's case it answers only to the family. The ownership architecture is different in each, but the purpose, permanence, is identical, and it is the same purpose that runs through every lasting fortune this series has examined.

Related reading

- To Act, Not to Seem: the Swedish foundation-control model these three echo.

- The Candy Fortune That Raises Two Thousand Children: a charitable trust controlling a public company, the Tata pattern in miniature.

- Two Percent of the Company, Forty Percent of the Vote: the supervoting share, Agnelli's device in an American setting.

- The Working Ledgers: the market and the money underneath every controlled empire.

Fact-check notes and sources

- Tata (the group's founding in 1868, its status as India's largest conglomerate with more than $180 billion in revenue and over $328 billion in listed market value, TCS as the roughly $30 billion financial engine, the Jaguar Land Rover and Corus acquisitions; the control structure in which the Tata Trusts hold about 66 percent of the unlisted holding company Tata Sons through the Dorabji and Ratan trusts and channel its dividends to philanthropy; Ratan Tata's 2024 death and the Noel Tata and Chandrasekaran successions; the 2016 Mistry ouster upheld in 2021; and the Shapoorji Pallonji minority stake and listing pressure): Tata, TCS, Jaguar Land Rover, Tata Steel, Tata Trusts, Al Jazeera, Business Standard, and iPleaders. The individual trust sub-percentages are press estimates because Tata Sons is unlisted.

- IKEA (Ingvar Kamprad's 1943 founding and 2018 death; the two-part structure in which Ingka Holding runs the retail business under the ownerless Stichting INGKA Foundation while Inter IKEA Systems owns the brand and collects a 3 percent franchise fee, now under a Liechtenstein foundation; the "owns itself" character of a stichting that makes IKEA unbuyable and unsplittable; the tax-minimizing design, the Swedish estimate of billions saved, and the 2017 EU state-aid investigation; and the family's capped minority role): Wikipedia, "Ingvar Kamprad", Ingka, Inter IKEA, Inter IKEA Foundation, Wikipedia, "Stichting INGKA Foundation", The Local, and European Commission. The roughly $36 billion foundation figure is a 2006 estimate and is dated.

- Agnelli (Giovanni Agnelli co-founding Fiat in 1899; the roughly two hundred family descendants controlling the empire through Giovanni Agnelli B.V. and the listed holding company Exor via special voting shares that yield about 55 percent of the economics but roughly 84 percent of the votes; Dicembre as John Elkann's apex vehicle; Exor's stakes in Ferrari, Stellantis, CNH, Juventus, Philips, and The Economist and the 2025 sale of Iveco to Tata Motors; Elkann as Exor's chief executive and the chairman of Stellantis and Ferrari; and Exor's roughly 33 billion euro net asset value and the family's roughly $14 billion estimated wealth): Exor history, Wikipedia, "Agnelli family", Exor ownership structure, SEC filing, Wikipedia, "Exor", GlobeNewswire, Exor on its chairman, and Exor NAV. Agnelli and Exor are controlled through a family holding company and loyalty shares, not a charitable foundation, a distinction this piece keeps explicit; Elkann is Exor's CEO, not its chairman.

This post is informational and historical, not financial advice. Figures are reproduced from the cited company, filing, and press sources, with estimates and dated figures flagged as such. Individuals and companies are discussed as nominative fair use from the public record, with no affiliation implied.